Note 41. The Congressional Budget Process, Briefly

Rules Matter, Rules Change

In the early 1970s interest in budget reform was spurred by chronic deficits and political tensions between the Democratic Congress and a Republican president. In retrospect, the deficits of that period seem small, but they were unprecedented for a time without a declared war. The shortfall was largely the result of the cost of President Lyndon Johnson’s Great Society program, spending on the Vietnam War, and the absence of compensating tax increases. Promising to gain control of the budget, Republican Richard Nixon won the 1968 presidential election and then proceeded to engage in battles with the Democratic Congress over spending and taxes. These battles motivated Congress to strengthen its own budget-making capacities by adopting the Congressional Budget and Impoundment Control Act of 1974, usually called the Budget Act.

Basics

The fiscal year for the federal government begins on October 1 and runs through September of the following year. For example, fiscal year 2020 starts on October 1, 2019, and ends on September 30, 2020. Thus, Congress aims to have spending and tax bills for the next fiscal year enacted by October 1 of each year. The president proposes a budget in February, leaving Congress less than eight months to act on it. Failure to pass bills that approve spending for federal agencies, called appropriations bills, may force a shutdown of some government agencies. In most such cases Congress passes continuing resolutions (CRs), which are joint resolutions of Congress that authorize temporary spending authority at the last year’s level or at some percentage of that level. Eventually, Congress passes appropriations bills or approves a year-long CR.

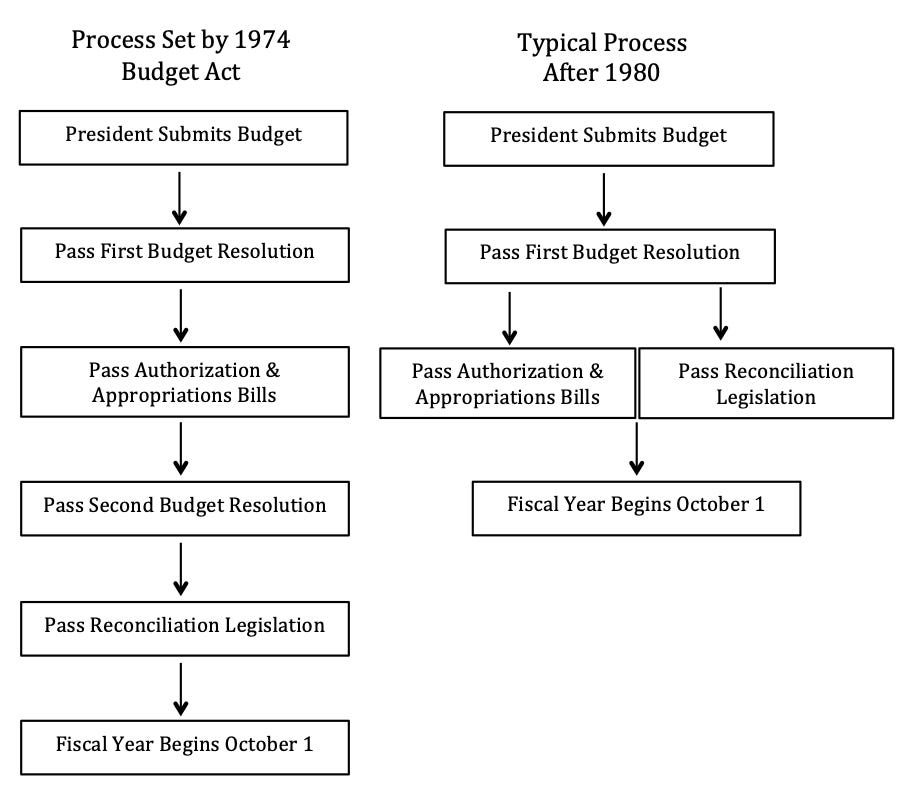

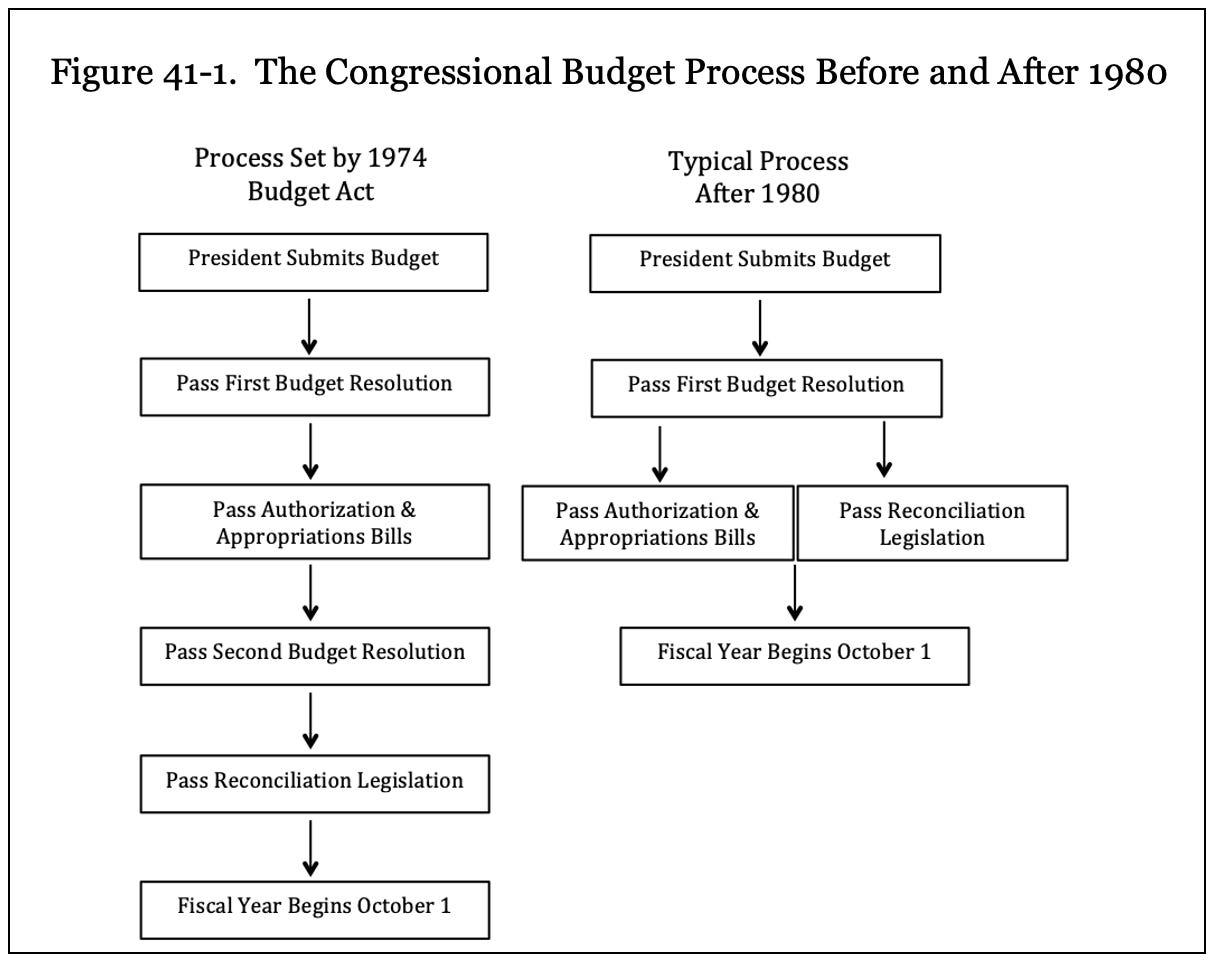

The Budget Act created a process for coordinating the actions of the appropriations, authorizing, and tax committees (left side of Figure 41-1). Each May Congress would pass a preliminary budget resolution setting nonbinding targets for expenditures and revenues. During the summer, Congress would pass the individual bills authorizing and appropriating funds for federal programs, as well as any new tax legislation. Then, in September, Congress would adopt a second budget resolution, providing final spending ceilings. This resolution might require adjustments to some of the decisions made during the summer months. Those adjustments would be reflected in the second resolution, and additional legislation, written by the proper committees, would then be drafted to make the necessary changes. This process of adjustment was labeled “reconciliation,” to reflect the need to reconcile the earlier decisions with the second budget resolution. The reconciliation legislation was to be enacted by October 1, the first day of the federal government’s fiscal year.

The Budget Act created two new committees, the House and Senate Budget Committees. The budget committees write the budget resolutions and package reconciliation legislation from various committees ordered to adjust the programs under their jurisdiction. The Congressional Budget Office (CBO) was created by the act to provide Congress with nonpartisan, expert analyses of the economy and budget.

The Senate accepted an important changes in its procedures as a part of the Budget Act. The act set a limit of twenty hours on debate over budget resolutions and reconciliation legislation. This meant that budget measures could not be killed by a Senate filibuster conducted by a minority of its members. Moreover, the act barred nongermane amendments when budget measures were considered on the Senate floor. Unlike most other legislation, senators could not use budget measures as vehicles for getting other matters to the House and the president. Advocates of the budget act successfully persuaded senators that establishing a budget process that had a reliable schedule and would not become side-tracked by fights over nonbudget issues was sufficiently important to compromise on traditional Senate practices.

Changing the Rules, Regularly

The new budget process worked smoothly during its first four years, primarily because the Democratic majorities in the House and Senate did not use budget resolutions to constrain or compel action from appropriations, authorizing, or tax committees. That did not last long. In 1979 and 1980, the last two years of the Carter administration, escalating deficits spurred a search for new ways to control spending. An effort in 1979 to include reconciliation instructions to committees in the second budget resolution ended in failure, in part because of resistance from some committees to reducing spending on programs under their jurisdiction. Confronting projections of a rapidly rising deficit, as well as a reelection campaign in 1980, President Carter and Democratic congressional leaders agreed to include reconciliation instructions in the first budget resolution, adopted in May. That is, at a point in the process before the usual authorization and appropriations legislation was considered later in the summer, they decided to order some committees to report legislation that would reduce spending to be incorporated in a reconciliation bill in June.

Moving reconciliation to earlier in the year meant that the initiative would shift from the various authorizing committees to the budget and party leaders, who together with administration officials would negotiate the reconciliation instructions. The innovation worked. The 1980 reconciliation legislation reduced the deficit by $8.2 billion through a combination of spending cuts and tax increases. Since then the term “reconciliation” has been used to describe any bill ordered by budget resolutions, although it no longer is limited to the originally intended process of reconciling the decisions of the summer months with the second budget resolution adopted just before October 1. In fact, since 1980 reconciliation, when used, has always been ordered by the first budget resolution, creating the process outlined on the right side of Figure 41-1.

The budget process was never again the process that was planned in 1974. Spending pressures in both domestic and defense programs, several major tax cuts, sharp partisan differences over spending and tax policy priorities, and divided party control of the House, Senate, and White House made budget issues a dominant issue in many Congresses. Deadlines imposed by appropriations, budget laws, and the need to raise the federal debt limit periodically created crises on many occasions. In most cases the response of party and budget leaders was to invent new rules governing future spending and tax decisions and the associated decision-making processes.

Congress experimented with many other rules and budget constraints to resolve political crises over spending and tax decisions. The major innovations in the budget process are listed in Table 41-1, which I have placed at the end of this Note. The innovations included:

caps on spending and floors on revenues,

sequestration (automatic across-the-board spending cuts if a maximum spending level or deficit is reached),

PAYGO (pay-as-you go, a process that required a spending increase to include compensating spending cuts),

mandatory review of entitlement spending, and

the creation of a temporary “super committee” charged with meeting certain deficit reduction goals (it failed).

Seldom did these inventions solve the political struggle over budgets. Each one, without exception, was modified or superseded by subsequent law as budgetary and political circumstances evolved.

One additional rule—known as the Byrd rule—deserves special notice because it remains an important limitation on what can be done in a reconciliation bill. In late 1986, in response to a stock market crash, Congress and President Ronald Reagan agree to spending ceilings for defense and nondefense spending for a two-year period. This compromise allowed the Reagan administration to end with a truce with Congress on the budget. Neither party was eager to continue the battle into the election year of 1988. The agreement gave Senator Robert C. Byrd (D-West Virginia), the outgoing majority leader and former Appropriations Committee chair, an opportunity to address his concerns about the abuse of reconciliation bills. Over the decade committees and even individual legislators attached legislative provisions unrelated to budgets and deficit reduction to reconciliation bills. Often, this was the easiest way to get some legislation through both houses and to the president. Byrd considered this a misuse of a process intended to put overall budgets in place and circumvented the normal Senate process that allowed free-standing bills, other than budget measure, to be filibustered.

The Byrd rule bars extraneous matter from reconciliation bills. A provision is considered to be extraneous if it does not change spending or revenues, concerns issues that lie outside of the jurisdiction of the committee reporting it, or leads to a net increase in spending or decrease in revenues for the years beyond those covered by the bill. In addition, strangely, any change in Social Security, Washington’s political sacred cow, is considered a violation of the Byrd rule.

The rule is enforced by points of order raised by senators from the floor and upheld by a ruling of the chair, who depends on the advice of the Senate parliamentarian. The Senate may overturn the ruling of the chair as long as sixty senators agree. If a point of order is successful, either through a ruling of the presiding officer or by a vote, the entire bill is ruled out of order. The rule gives a sizable minority the ability to prevent certain kinds of provisions from being included in reconciliation bills. It is one of the few places in which Senate rules are more restrictive than House rules. Since its adoption the Byrd rule has been an obstacle to the inclusion of many legislative provisions that are tangential to the budget purposes of reconciliation bills, including the Republican effort to repeal the Affordable Care Act (Obamacare) in 2017.

Strategic Packaging of Tax Bills

Until the late twentieth century Congress usually considered tax legislation in bills recommended by the House Ways and Means and Senate Finance committees. Because the Constitution requires that revenue bills originate in the House, a Ways and Means tax bill would be first considered in the House, usually under a closed rule, a rule that prohibits the consideration of amendments. The Senate bill would be debated and passed, and a conference committee, comprised of legislators from Ways and Means and Finance would devise a final version that would be approved by the House and Senate. Filibusters were seldom a problem in the Senate on the Senate bill or the conference report.

Since the 1980s increasing partisan tensions and more credible threats of minority party filibusters in the Senate has motivated innovations in the legislation process of passing tax legislation In fact, over the last decade no major tax bill has made it through Congress using the standard process. Instead, one of three different processes have been used.

One route is a hybrid of the standard legislative process, but, rather than working strictly with committee-written bills, key provisions are negotiated between the president and top party leaders, along with committee leaders, and the legislation is amended with the compromise provisions and adopted by the House and Senate without a conference committee. A major tax bill enacted in 2012, extending major tax cuts that were going to expire under current law but setting caps on certain deductions and credits, was negotiated by Vice President Joe Biden, representing the Obama White House, and then–Senate Minority Leader Mitch McConnell. Their handiwork was adopted as an amendment to the pending legislation and approved through an exchange of amendments between the House and Senate.

A second route is to incorporate tax provisions in a larger reconciliation bill. Since the early 1980s reconciliation bills aimed at reducing deficits have included provisions that both cut spending and increased revenues. Because reconciliation bills and their conference reports are considered under debate and amendment limits in both houses, and therefore protected from filibusters in the Senate, tax bill advocates learned to use reconciliation as a means to gain action on their proposals. Many reconciliation bills included tax provisions as a part of larger reconciliation bills and were approved by simple majorities in both houses.

A third route is to label an entire tax-cut measure a reconciliation bill and do nothing else in that bill. This was first done in 1999 and was followed by major tax-cut measures in 2001, 2003, and 2017. As for other budget measures, these tax-oriented reconciliation bills allowed House and Senate majorities (Republican majorities in all four cases) to avoid Senate filibusters and certain kinds of floor amendments. These moves have been controversial. Reconciliation bills, in the view of some observers, should concern efforts to reduce the deficit, but the tax-cut measures, while related to the budget, were projected to reduce projected revenues and increase deficits. The use of reconciliation for tax cuts was determined to be permissible, but the Byrd rule’s requirement that a reconciliation bill cannot increase the deficit for the years beyond the next ten years forced the adoption of sunset provisions on major tax cuts. When the sunset provisions were added to the 2003 tax cuts, it guaranteed the controversial tax legislation would be reconsidered in another decade.

Strategic Packaging of Authorization Bills

Because reconciliation bills cannot be filibustered in the Senate, legislators are tempted to squeeze new policy initiatives into reconciliation bills, even when those bills will increase federal spending. The Byrd rule still applies, but the Budget Act allows Congress to address mandatory (entitlement) spending (except Social Security). This gives advocates the opportunity to use reconciliation on a range of health, welfare, and education programs. A reconciliation bill completed work in creating Obamacare in 2010 and another was used to enact COVID-19 relief in the American Rescue Plan of 2021. In 2022, a major infrastructure and climate change bill was enacted as a reconciliation bill. This route can be used as long as Congress passes a budget resolution that authorizes a subsequent reconciliation bill and specifies the committees that are to produce components of the bill. That requires planning and House-Senate agreement, which usually dooms reconciliation as a path to legislating when the two houses are controlled by different parties.

Rules Matter, Rules Change

The history of the budget process illustrates important features of congressional politics and procedure. Rules matter, and the players in the legislative game frequently change the rules to meet new political circumstances. The Budget Act of 1974 altered the traditional relationship between the parent houses and their committees, and then it was amended many times to restructure the process, set constraints on spending and revenue decisions, and establish mechanisms to enforce budget agreements. Partisan conflict motivated many of these developments, but factions within each party often insisted on procedural changes that would advance their policy interests.

Table 41-1. Major Developments in the Budget Process, 1974–2019

1974 Congressional Budget and Impoundment Control Act

Created the modern budgeting process, established the budget committees, and provided for congressional review of presidential rescissions and deferrals.

1980 Reconciliation Bill

Provided that (for the first time) reconciliation be used at the start of the budget process. Committees were required to forward legislation drafted specifically to reduce spending as required by the first budget resolution.

1985 and 1987 Gramm-Rudman-Hollings Rules

Set fixed annual targets for deficit reduction and established a sequestration process to bring spending down to levels required to meet targets.

1990 Budget Enforcement Act

Dropped the fixed deficit targets of the Gramm-Rudman-Hollings approach and replaced them with caps on spending in domestic, defense, and international budgetary categories; PAYGO (pay-as-you-go) rules for spending and revenues that require new spending to be offset by equal spending cuts or tax increases; and restrictions on loans and indirect spending.

1993 Omnibus Budget Reconciliation Act

Modified spending priorities and extended the enforcement provisions of the 1990 act through 1998.

1996 Balanced Budget Act

Modified spending priorities, extended the enforcement provisions of the 1993 act through 2002, and projected a balanced budget in fiscal year 2002.

2002

PAYGO enforcement provisions allowed to expire.

2007

PAYGO rule adopted; rules requiring sponsors of earmarks to be identified; House rule provides a “trigger” that establishes a point of order against tax-cut legislation that does not require that the Office of Management and Budget certify that the tax cuts cost less than $179.8 billion through fiscal 2012 or more than 80 percent of any surplus projected for 2012 at the time.

2009

PAYGO rule changed in the House to align it with the rule in the Senate so that both chambers use the same CBO baseline to assess compliance, to allow separate House-passed bills to be considered collectively deficit neutral provided that they are linked at engrossment, and to include an emergency exception to the PAYGO rule; rule providing a point of order against any earmark inserted in a general appropriations conference report.

2010

The National Commission on Fiscal Responsibility and Reform, a presidential commission, produced a nonbinding plan for discretionary and mandatory spending caps, budget process reforms to enforce the caps, and tax changes to reduce rates, broaden the tax base, and eliminate tax breaks.

2011

The House, with a new Republican majority, adopted the “CutGo” rule, which requires that new mandatory spending be offset with cuts to existing programs (i.e., cannot be offset with revenue increases); placed funding cut from appropriations bills through floor amendments in a separate account so that it cannot be used for other purposes; eliminated the “Gephardt rule,” which provided for automatic approval of a debt limit measure upon adoption of a budget resolution by both houses; and gave the Budget Committee chair the authority to set spending caps for the remainder of fiscal 2011. The Budget Control Act of 2011 reinstituted sequestration for a ten-year period, totaling $1.2 trillion in spending cuts equally divided between defense and domestic programs.

2011

Congress created a “super committee” charged with meeting certain deficit reduction targets by a specified date. Failure to meet the deadline would trigger spending caps on defense spending that the Republicans would find unacceptable and nondefense spending caps that the Democrats would find unacceptable. The committee failed and caps considered to be quite severe were put in place for a ten-year period. The caps have been modified several times. At this writing in 2019, we are in the second year of a two-year agreement on defense and nondefense spending caps that both parties approved in 2017.

2015

The House adopted a “dynamic scoring” rule that requires the CBO to estimate the effect of major legislation by taking into account “macroeconomic effects” in making cost estimates, a rule intended to make tax cuts more attractive.

2019

The House, with a new Democratic majority, eliminated the CutGo rule to restore the PAYGO rule; reinstituted a new Gephardt rule that provides for automatic approval of a debt limit measure upon adoption of a budget resolution by just the House; and eliminated the “dynamic scoring” rule.

2023

As a part of a debt ceiling agreement between a House Republican majority, Senate Democratic majority, and Democratic President Joe Biden, Congress agreed to set caps on domestic and defense discretionary spending for two years. The new Republican majority repealed the Gephardt rule.